The artificial intelligence investment story is no longer only about GPUs. High-bandwidth memory has become one of the most important constraints in an AI server, turning SK Hynix and Micron into two of the market's most closely watched semiconductor companies. This analysis compares their technology, growth, valuation logic, risks, and the evidence that could change the investment verdict.

Executive Summary

SK Hynix and Micron Technology are both direct beneficiaries of the AI infrastructure boom, but they offer investors two different versions of the same thesis. SK Hynix is the established high-bandwidth memory leader. Its early execution in HBM3 and HBM3E gave it a privileged position in the supply chain for advanced AI accelerators, and that advantage translated into record financial results. Micron is the challenger. It has a smaller position in HBM, but it is expanding rapidly, has secured customers for its latest products, and offers U.S. investors a familiar Nasdaq-listed vehicle with transparent SEC reporting.

The central question is not whether AI will require more memory. It almost certainly will. The harder question is how much of that demand has already been reflected in expectations, how durable today's unusually favorable pricing can be, and whether HBM has permanently improved memory economics or merely produced an exceptional peak in a historically cyclical industry.

SK Hynix currently has the stronger operating position. It has greater HBM scale, deeper production experience, and a demonstrated ability to convert technical leadership into high margins. If an investor wants the company with the clearest competitive advantage today, SK Hynix is the more convincing answer. Micron, however, may offer more upside if it closes the technology and market-share gap without triggering destructive industry supply growth. Its challenger status creates greater execution risk, but it also means that successful share gains can produce a larger change in earnings expectations.

Our base-case conclusion is therefore conditional rather than absolute: SK Hynix is the higher-quality pure expression of the HBM leadership thesis, while Micron is the more accessible catch-up thesis with greater potential sensitivity to improving market share and margins. Investors should not choose between them by looking only at trailing share-price performance. They should track HBM qualification, customer concentration, capital expenditure, conventional DRAM pricing, yields, free cash flow, and the pace at which new capacity enters the market.

Why the AI Memory Trade Is Back in Focus

Semiconductor investors spent the first stage of the generative AI boom concentrating on the companies that design accelerators. That focus was understandable. The GPU became the visible symbol of the AI data center, and Nvidia became the primary beneficiary. But an accelerator cannot work in isolation. Large models require enormous volumes of data to move rapidly between memory and computing cores. When that transfer is too slow, expensive processors wait for data instead of performing useful calculations.

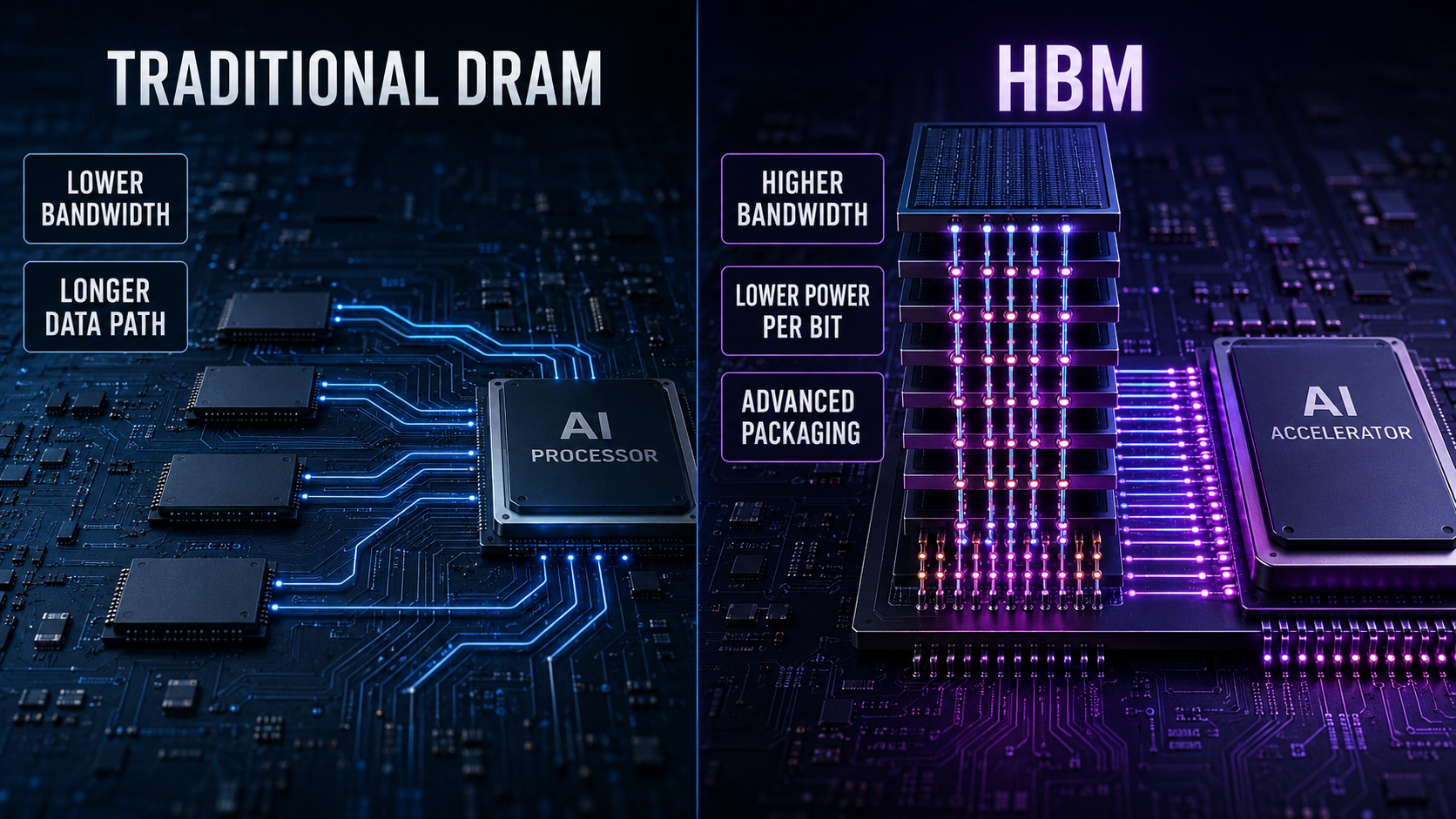

That bottleneck is why high-bandwidth memory matters. HBM stacks multiple DRAM dies vertically and connects them through advanced packaging. The structure provides much higher bandwidth and better energy efficiency than conventional memory arrangements, but it is also more difficult to design, manufacture, test, and package. Each new generation pushes density, bandwidth, thermals, power consumption, and yield requirements further. The product is therefore not simply ordinary DRAM sold at a higher price. It combines memory technology, packaging expertise, manufacturing discipline, and close collaboration with accelerator customers.

The market's renewed attention followed a period of conflicting signals. AI-related semiconductor stocks rallied on expectations for continued infrastructure spending, then sold off when investors questioned whether capital expenditures and memory pricing could remain elevated. That disagreement is useful. A stock is most interesting when reasonable analysts can observe the same facts and reach different conclusions.

The bullish side sees a structural transformation. Larger models, more inference, multimodal applications, agentic systems, and increasingly complex accelerators require more memory per system. HBM supply is negotiated far in advance, qualification cycles are demanding, and leading suppliers have limited ability to add advanced capacity quickly. In that view, the industry has gained visibility, pricing power, and customer commitment that were largely absent in older memory cycles.

The bearish side sees familiar ingredients beneath a new label. Memory remains capital intensive. High prices encourage investment. Investment creates supply. Supply eventually catches demand, and pricing falls faster than consensus expects. Even if AI demand continues growing, shareholders can still lose money when expectations, valuation, or capacity expand faster than end demand. The existence of a powerful technology trend does not eliminate the possibility of a poor entry price.

What Makes HBM Economically Different From Traditional DRAM?

Traditional memory has often behaved like a commodity. Suppliers invest during strong markets, customers build inventory, and prices rise. Eventually new capacity arrives or demand slows. Customers reduce purchases, inventory accumulates, prices collapse, and manufacturers cut capital expenditure. The cycle then begins again. Product differentiation exists, but supply and demand have historically exerted enormous influence over profitability.

HBM changes several parts of that model. First, the product is technically complex and tightly connected to the customer's accelerator roadmap. A memory stack must meet specific requirements for bandwidth, capacity, power, heat, packaging, and reliability. Qualification can take time, and a failed qualification can exclude a supplier from an important product cycle.

Second, HBM consumes more manufacturing resources than standard DRAM. Stacking dies, using through-silicon vias, and completing advanced packaging create additional steps and yield challenges. The opportunity cost matters because allocating more wafer capacity to HBM can tighten supply in conventional DRAM. A surge in HBM demand can therefore support broader memory pricing even before HBM represents the majority of industry bits.

Third, purchasing agreements can be discussed much earlier than in the conventional spot-oriented memory market. Both major suppliers have described substantial customer commitments for future HBM production. These agreements improve visibility, although investors should not treat every forecast or discussion as an unconditional, risk-free contract. Volumes, specifications, timing, pricing adjustments, and qualification milestones still matter.

Fourth, the product roadmap is accelerating. HBM3E is followed by HBM4, then customized variants and future generations. Leadership is not secured forever by winning one generation. The supplier must execute repeatedly as customers demand more layers, greater bandwidth, better efficiency, and increasingly customized logic. This creates a genuine moat for the best operators, but it also creates a constant risk of technical disruption.

These differences make HBM more attractive than legacy commodity memory, but they do not abolish cyclicality. HBM is still produced in expensive fabrication plants. Customers can revise capital plans. Competing suppliers can improve yields. New accelerator architectures can change the mix of memory required. The correct conclusion is not that the cycle has disappeared. It is that the duration, visibility, margins, and competitive structure of the cycle may be better than they were in the past.

SK Hynix: The Current HBM Leader

SK Hynix entered the AI boom with the most valuable asset a memory manufacturer could possess: proven HBM execution at scale. Its relationship with leading accelerator platforms and its ability to supply advanced generations allowed it to capture the early economics of the market. According to a 2026 market outlook published by the company and citing Counterpoint Research, SK Hynix held 62% of HBM shipments in the second quarter of 2025 and 57% of HBM revenue in the third quarter of that year. Market-share estimates vary by methodology, but the direction is clear: SK Hynix began this phase as the leader.

That leadership showed up in reported results. SK Hynix announced fiscal 2025 revenue of KRW 97.1467 trillion, operating profit of KRW 47.2063 trillion, and net profit of KRW 42.9479 trillion. The reported operating margin was 49%. Revenue increased by more than KRW 30 trillion from 2024, while operating profit nearly doubled. These are extraordinary figures for a company operating in an industry once associated with violent profit swings and weak pricing power.

The financial improvement was not produced by HBM alone. Strong server demand, favorable conventional memory pricing, enterprise SSD products, and disciplined product allocation also helped. Still, HBM was the strategic center of the transformation. It improved product mix, absorbed production resources, and strengthened the company's position with the most important AI infrastructure customers.

SK Hynix also moved aggressively into HBM4. The company said it completed development of a 12-layer HBM4 product in 2025, with twice the number of input/output channels of the previous generation and a significant improvement in power efficiency. Technical claims from a manufacturer should always be tested against customer qualification and mass-production results, but early product readiness matters. Each generation gives the leader another opportunity to preserve its installed relationships and production learning.

The Bull Case for SK Hynix

The strongest bullish argument is that SK Hynix has already demonstrated the combination of technology and manufacturing needed to win. In semiconductors, a presentation slide is not the same as high-volume production. A company must deliver qualified products, maintain yields, scale packaging, and meet customer schedules. SK Hynix has accumulated experience that cannot be reproduced instantly by announcing higher capital expenditure.

Its scale may also create a learning advantage. Higher volume produces more manufacturing data, which can improve yields and process control. Better yields lower unit costs and make it easier to supply customers profitably. Large customers prefer dependable suppliers because a shortage of one memory component can delay an entire accelerator system. Reliability therefore reinforces commercial relationships.

The second bullish argument is that AI demand is expanding beyond training. Training a frontier model attracts attention, but inference can become an even larger workload as millions of users and businesses run models continuously. Reasoning models use additional test-time computation. Multimodal systems process text, images, audio, and video. Agents can execute repeated steps rather than answer a single prompt. These trends increase the amount of computation and memory traffic associated with each useful AI outcome.

The third argument is supply discipline. Advanced HBM capacity cannot appear overnight. Clean-room construction, equipment installation, process migration, packaging capacity, substrate availability, and yield improvement all require time. If demand remains strong while supply expansion remains measured, SK Hynix can preserve attractive pricing and margins longer than a conventional memory-cycle model would imply.

Finally, SK Hynix offers exposure beyond a single HBM generation. Its broader DRAM portfolio, enterprise SSD capabilities, and participation in next-generation AI memory formats allow it to benefit from the overall growth of data-center memory. The company is not merely selling one component into one accelerator. It is attempting to become a full-stack AI memory supplier.

The Bear Case for SK Hynix

The greatest risk is that the market already understands the story. A dominant market position, record margins, and visible AI demand can attract a valuation that assumes continued perfection. When expectations become high enough, good operating results may no longer be sufficient. The company must beat a rising bar while preserving its technical lead.

Customer concentration is another concern. The AI accelerator market itself is concentrated, so leadership can produce dependence on a small number of buyers. A change in qualification, product architecture, sourcing policy, or negotiating leverage at one major customer can have an outsized effect. Long relationships are valuable, but large customers also have strong incentives to cultivate alternative suppliers.

Competition is intensifying. Micron is expanding its HBM portfolio, and Samsung has the financial resources, manufacturing scale, and strategic motivation to recover share. SK Hynix does not need to lose leadership for its economics to weaken. A shift from scarcity to adequate supply could pressure pricing, even if the company remains number one.

Capital intensity is also unavoidable. The company must invest to keep its lead, build capacity, and prepare for new generations. During a strong market, large capital expenditure looks rational. If demand later disappoints, depreciation continues while utilization falls. Free cash flow can therefore change more sharply than operating profit at the top of a cycle.

Investors outside South Korea must additionally consider trading structure, currency exposure, disclosure conventions, taxation, and the difference between local shares and any U.S.-traded instrument available to them. Accessibility can affect liquidity and valuation. The quality of the underlying company does not eliminate these portfolio-level considerations.

Micron: The Challenger With Operating Leverage

Micron occupies a different position. It is not the historical HBM leader, but it has become increasingly relevant as customers seek qualified supply and as its products improve. The company has emphasized performance and power efficiency, expanded its HBM customer base, and secured commitments for future production. In December 2025, Micron said it had completed price and volume agreements for its entire calendar 2026 HBM supply, including HBM4. It also projected the HBM total addressable market would grow from approximately $35 billion in 2025 to around $100 billion in 2028.

That forecast implies roughly 40% annualized market growth over the period. Forecasts this aggressive should not be accepted uncritically, especially when they come from a direct beneficiary. Nevertheless, the projection illustrates the scale of the opportunity management is planning for. Micron believes HBM can become larger by 2028 than the entire DRAM market was in calendar 2024.

Micron's broader financial momentum has also been strong. In its fiscal 2026 materials, the company reported records across revenue categories and described strong data-center and HBM demand. Its fiscal third-quarter commentary emphasized the strategic value of memory in the AI era and the role of multi-year customer agreements in making performance more durable and predictable.

For U.S. investors, Micron has another practical advantage: it trades directly on Nasdaq and reports under U.S. securities rules. That accessibility makes it easier to own, compare, hedge, and include in institutional portfolios. It also means the stock is already widely followed, so accessibility should not be confused with informational inefficiency.

The Bull Case for Micron

The most compelling bullish argument is operating leverage from a lower starting share. A leader must defend a large position; a challenger can create substantial incremental revenue by winning a few programs or expanding allocations. If Micron's HBM4 execution is strong and customers deliberately diversify supply, its share can rise even while the total market expands rapidly.

Customer diversification is a rational industry objective. Accelerator designers do not want to depend permanently on one memory supplier. Qualifying Micron can improve supply security and negotiating leverage. This does not guarantee equal allocations, because customers will still prioritize performance, yield, and reliability. But it creates a structural reason to support a credible second source.

Micron also benefits from HBM's effect on the conventional DRAM market. Because HBM consumes significant wafer and packaging resources, growing HBM output can limit the capacity available for ordinary products. Even when Micron does not capture the leading HBM share, tighter DRAM supply can support selling prices across its portfolio. The investment case is therefore broader than HBM revenue alone.

Another advantage is technological ambition. Micron has presented its recent HBM products as competitive in power and performance and expects faster yield maturation for HBM4 than it achieved with HBM3E. If that expectation is fulfilled, the company can improve costs while scaling volume. Yield improvement is one of the most important variables because a technically impressive product can still produce disappointing economics if too many units fail.

Finally, Micron can benefit if the market underestimates the duration of the memory upcycle. Earnings estimates for memory companies often lag rapid price movements. When pricing, utilization, mix, and yields improve simultaneously, profits can increase much faster than revenue. That same leverage works in reverse, but it creates significant upside during a favorable phase.

The Bear Case for Micron

Micron's catch-up thesis depends on execution that has not yet been demonstrated at the same scale as SK Hynix. Customer agreements are encouraging, but actual shipments, qualification, yields, and margins determine shareholder value. A delay in HBM4 or weaker-than-expected yields could push revenue into a later period while expenses and capital spending continue.

The company also faces a difficult strategic balance. It must invest enough to gain share, but not so aggressively that industry capacity destroys pricing. Individual companies often describe their spending as disciplined, yet the combined actions of several rational competitors can still create oversupply. Investors must analyze industry-wide additions, not only Micron's stated intentions.

Micron remains exposed to conventional memory cycles, consumer electronics, inventory adjustments, and geopolitical constraints. AI data centers are increasingly important, but they do not erase every other end market. Weakness in PCs, smartphones, autos, industrial demand, or NAND can partially offset HBM strength.

There is also a valuation trap that appears frequently in cyclical stocks. A memory company can look statistically cheap near peak earnings because the denominator in the price-to-earnings ratio is temporarily elevated. Investors who buy only because a trailing multiple is low may discover that profits fall faster than the share price. Normalized margins and mid-cycle free cash flow are more informative than a single peak-year multiple.

SK Hynix vs. Micron: Side-by-Side Comparison

FactorSK HynixMicronCurrent Edge HBM market positionEstablished leader with large share and proven scaleCredible challenger expanding allocationsSK Hynix Execution evidenceStrong track record across recent HBM generationsImproving products, but smaller scaleSK Hynix Share-gain potentialMust defend a large baseCan grow rapidly from a smaller baseMicron U.S. investor accessibilityRequires attention to available trading structureDirect Nasdaq listing and SEC reportingMicron Customer diversification catalystIncumbent relationships are a strengthBenefits when customers qualify second sourcesMicron Current competitive moatScale, know-how, qualification, and customer trustTechnology progress and manufacturing footprintSK Hynix Upside sensitivityDriven by maintaining leadership and market growthDriven by market growth plus successful catch-upMicron Execution riskRisk of losing some leadRisk of delayed qualification or weak yieldsSK Hynix

This comparison explains why the answer depends on portfolio objectives. A quality-focused investor may prefer the proven leader. An investor seeking positive estimate revisions from market-share gains may prefer the challenger. Neither framing removes the need to examine entry valuation.

The Technology Race: HBM3E, HBM4, and Customization

Investors can become distracted by generation labels. A new product name sounds decisive, but the commercial process has several stages: development, sampling, customer qualification, volume production, yield stabilization, and profitable shipment. Announcing HBM4 is not the same as shipping it at scale, and shipping at scale is not the same as earning an attractive return on the capital required.

HBM4 is important because it increases the interface width and raises the requirements for bandwidth and efficiency. It also moves the market toward greater customization. As base dies become more sophisticated and customers optimize memory for specific accelerators, collaboration can deepen. This may reduce pure commoditization and create switching costs, but it can also increase research expense and customer concentration.

SK Hynix's advantage lies in its established learning curve. It has experience integrating advanced stacks into leading accelerator platforms and navigating production challenges. Micron's opportunity lies in using newer processes and designs to narrow the gap. A challenger does not always need to copy the leader's path; it can sometimes reach competitive economics with a different combination of process technology, die size, power efficiency, packaging, and customer support.

The correct way to assess the race is not to count press releases. Investors should watch qualification announcements tied to named platforms, shipment timing, the number of customers, HBM revenue, gross-margin progression, capital intensity, and management commentary about yields. When a company claims superior efficiency, the relevant follow-up question is whether customers accept the product and whether the supplier can manufacture it profitably.

Does Nvidia Dependence Strengthen or Weaken the Thesis?

Nvidia's dominance has helped create the HBM opportunity. Its accelerators require enormous memory bandwidth, its system roadmaps influence supplier qualification, and its rapid product cadence supports demand for new HBM generations. A strong relationship with Nvidia is therefore an obvious asset.

Apply this research method to your stock

Generate bull/bear views, risk notes, and an evidence trail for SK.

But concentration creates asymmetry. If one customer represents a large portion of premium demand, that customer can influence specifications, allocation, timing, and price. It can also encourage multiple suppliers. The better the economics become for memory vendors, the stronger the customer's incentive to diversify and negotiate.

Custom AI chips complicate the picture but do not automatically reduce HBM demand. Google, Amazon, Meta, and other hyperscalers are developing internal accelerators. Some investors view those chips as a threat to Nvidia and therefore to Nvidia-linked suppliers. Yet custom accelerators also require high-performance memory. If total AI computation grows, a more diverse accelerator market can expand the addressable customer base for HBM.

The risk is architectural, not merely competitive. Different chips can use different memory configurations. Cost-optimized inference systems may use less expensive memory in some workloads. Improvements in model efficiency, quantization, caching, networking, or software can reduce memory required per task. Investors should therefore focus on total HBM content and units across the ecosystem, not only the market share of one accelerator designer.

Valuation: Why the Simplest Multiple Can Mislead

A precise valuation comparison requires current share prices, share counts, net cash or debt, forward estimates, and a consistent treatment of currencies and accounting periods. Those inputs change constantly. More importantly, applying a single price-to-earnings multiple to peak profits can create false confidence.

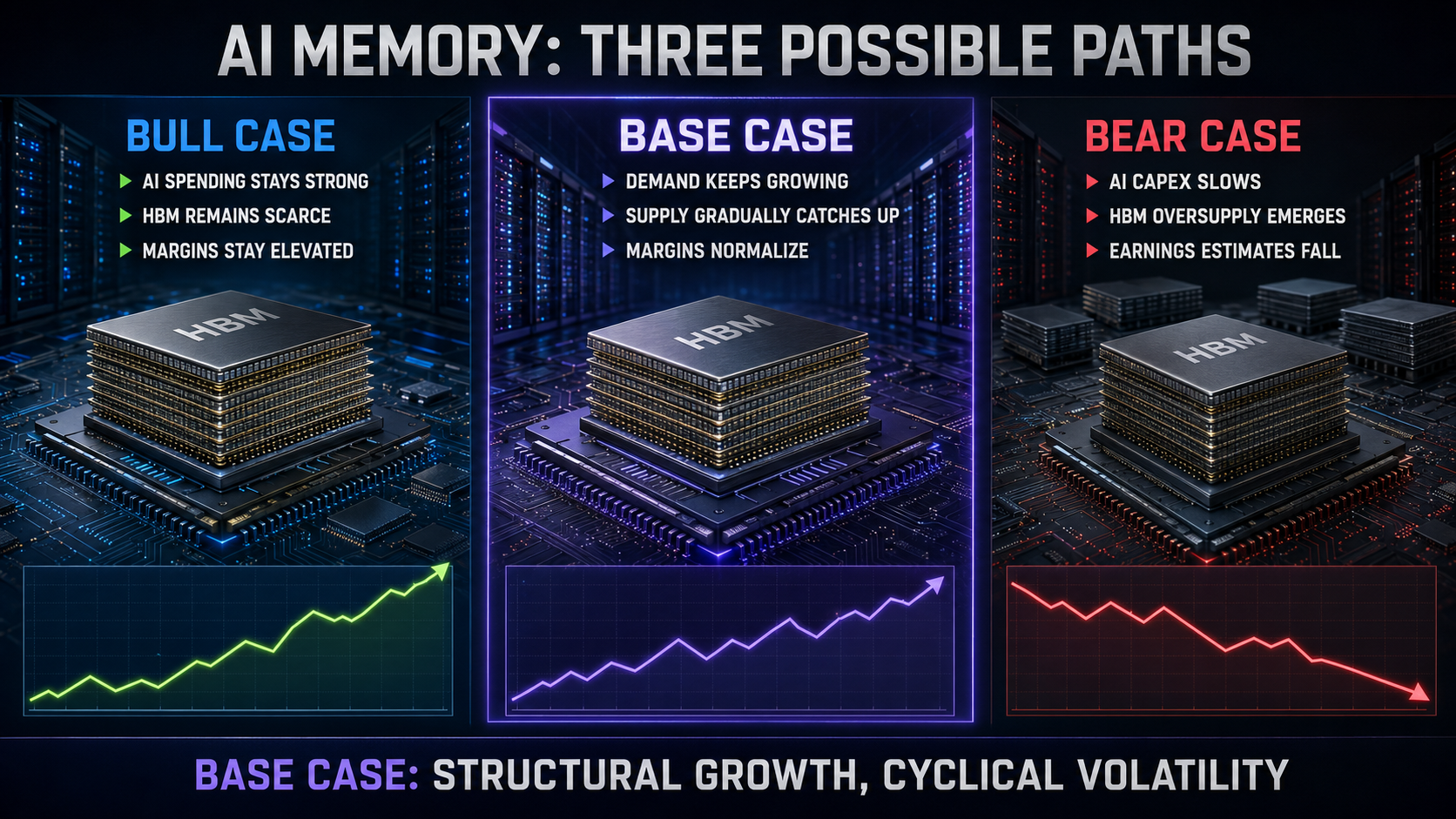

A better framework separates three scenarios. In a bear case, AI capital expenditure slows, HBM supply expands, conventional DRAM prices weaken, and margins normalize sharply. In a base case, HBM demand continues growing, pricing moderates gradually, and leading suppliers retain better margins than in historical cycles. In a bull case, compute demand continues to surprise, HBM remains scarce, customization raises barriers, and free cash flow compounds despite high investment.

For SK Hynix, valuation should reflect the durability of leadership. A premium is reasonable if the company can defend its share, execute HBM4, and keep returns structurally above its historical average. That premium becomes dangerous if it assumes that current margins are permanent.

For Micron, valuation should reflect both catch-up potential and execution risk. The stock deserves a higher normalized earnings estimate if HBM raises its product mix and reduces volatility. It does not deserve full credit for future share until qualification, shipments, and yields confirm the story.

Investors should calculate enterprise value against normalized operating profit, free cash flow after capital expenditure, and replacement cost. They should also examine price-to-book value because memory manufacturing requires a large asset base. No single measure is sufficient. A low P/E can be a peak-cycle warning, while a high P/E can occur near a trough when earnings are temporarily depressed.

Five Variables That Matter More Than the Headline P/E Ratio

1. HBM Revenue and Mix

Growth is more valuable when it changes the quality of earnings. Investors should track the portion of DRAM revenue coming from HBM and other premium products, not merely total bit shipments. A higher-value mix can support margins even if unit growth slows.

2. Gross Margin and Yield

Gross margin reveals whether technical success is becoming economic success. Improving HBM yields can lower costs rapidly. Falling margins despite strong revenue may indicate price pressure, poor yields, expensive ramp costs, or weakness elsewhere in the portfolio.

3. Capital Expenditure

Capital expenditure is both a growth signal and a future supply risk. Spending can support advanced-node transitions and packaging expansion, but aggressive industry-wide spending raises the probability of oversupply. Compare capex with depreciation, revenue, free cash flow, and expected bit growth.

4. Customer Commitments

Forward agreements can stabilize visibility, but investors should distinguish between completed pricing and volume agreements, broad customer discussions, and nonbinding forecasts. They should also watch whether commitments extend across multiple customers and generations.

5. Conventional DRAM and NAND Pricing

HBM receives the headlines, but the rest of the portfolio still matters. Strong conventional prices amplify the AI thesis; a collapse can offset HBM gains. NAND has different supply dynamics and can create additional volatility.

The Bull Case for the Entire AI Memory Industry

The strongest industry bull case begins with compute growth. AI models are becoming more capable, but capability often requires more inference steps, larger context windows, multimodal inputs, and greater memory traffic. Efficiency gains lower the cost of each task, which can increase total usage through a rebound effect. Cheaper intelligence may lead businesses to run far more queries rather than spend less overall.

Second, AI infrastructure is becoming strategically important to governments and corporations. Cloud providers, sovereign projects, model laboratories, and enterprises do not want to fall behind. Strategic spending can remain strong even when near-term returns are difficult to measure, extending the investment cycle.

Third, memory content per accelerator and per system can grow. More powerful chips need higher bandwidth and larger capacity. At the rack level, networking, storage, and memory requirements can rise alongside compute. This means HBM suppliers can grow even without relying solely on higher accelerator unit shipments.

Fourth, the supplier base is concentrated. Only a few companies can manufacture advanced DRAM, and fewer can execute cutting-edge HBM at scale. Barriers include intellectual property, fabrication expertise, packaging, customer qualification, equipment, and capital. A concentrated structure can support better returns if competitors remain disciplined.

Finally, customization may create longer and deeper customer relationships. As memory becomes more integrated with accelerator design, suppliers can participate earlier in product roadmaps. This improves visibility and makes last-minute substitution harder. The industry may evolve away from purely interchangeable products toward co-designed components with differentiated economics.

The Bear Case: Why a Great Technology Can Still Be a Bad Investment

The bear case starts with expectations. AI is not a hidden theme. Investors, suppliers, customers, and governments are committing enormous capital to it. When consensus becomes extremely optimistic, the market may price several years of successful execution in advance. A company can grow rapidly while its stock underperforms because valuation compresses.

Second, hyperscaler capital expenditure must eventually produce returns. Cloud companies can fund large programs today, but shareholders will demand evidence of revenue, margin, and cash generation. If AI monetization disappoints, spending plans can be delayed. Memory suppliers sit upstream, so order changes can propagate through the supply chain.

Third, supply responses are inevitable. SK Hynix, Micron, and Samsung all want to capture the opportunity. Packaging companies, equipment vendors, and governments are supporting expansion. Capacity is slow to build, but a delayed supply wave can still arrive after demand growth moderates.

Fourth, technology can reduce resource intensity. Better models, compression, quantization, sparsity, optimized inference, and improved memory management may reduce the hardware needed for a given output. These improvements do not necessarily shrink the total market, because usage can expand, but they introduce uncertainty into simple extrapolations.

Fifth, geopolitics can affect equipment access, customer markets, subsidies, export rules, and manufacturing locations. Memory is strategically important and globally interconnected. A change in trade policy can alter demand or costs without changing the underlying AI technology.

Finally, historical memory cycles deserve respect. Every cycle has a persuasive story at the top. This one has stronger structural foundations than many previous cycles, but the burden of proof remains with those claiming that supply-and-demand economics have been permanently repealed.

Where the SK Hynix Thesis Could Break

The SK Hynix investment thesis would weaken materially if several indicators appeared together. The first would be a loss of qualification or allocation on a major next-generation accelerator platform. A single program loss would not destroy the business, but it would challenge the assumption that leadership automatically carries forward.

The second would be HBM revenue growth accompanied by falling gross margin and rising capital intensity. That combination could indicate that competition is shifting value from suppliers to customers or that manufacturing complexity is consuming the expected premium.

The third would be aggressive market-share gains by both Micron and Samsung. SK Hynix can tolerate some diversification while the total market grows, but simultaneous share pressure and price pressure would undermine the premium-quality thesis.

The fourth would be a sustained decline in hyperscaler capital-expenditure expectations or accelerator orders. Temporary pauses are normal. A broad multi-quarter reduction across customers would be more serious.

The fifth would be evidence that advanced HBM capacity is becoming abundant earlier than expected. Shorter lead times, weaker forward pricing, customer inventory growth, and reduced urgency in supply agreements would all matter.

Where the Micron Thesis Could Break

Micron's thesis would weaken if its HBM4 ramp missed customer schedules or failed to achieve expected yields. Because the stock's upside includes a catch-up assumption, delays can have a disproportionate effect on forward estimates.

A second warning would be heavy capital spending without corresponding HBM revenue and margin improvement. Investment must create qualified output and cash flow, not merely capacity.

A third would be evidence that customers continue to treat Micron primarily as a secondary supplier with limited allocations. Diversification creates an opening, but the company must convert qualification into meaningful volume.

A fourth would be conventional DRAM or NAND weakness severe enough to overwhelm HBM gains. Investors should not mistake one fast-growing product line for immunity from the rest of the memory market.

A fifth would be expanding industry capacity combined with Micron's pursuit of share. A challenger is tempted to price aggressively. If several suppliers chase volume simultaneously, the resulting market can punish everyone.

Scenario Analysis: What Could Happen Next?

Bull Scenario

AI infrastructure spending remains stronger for longer. Reasoning and agentic workloads expand inference demand, next-generation accelerators increase HBM content, and supply remains constrained by packaging and yields. SK Hynix preserves leadership, while Micron gains enough share to grow faster without causing severe price competition. Both companies generate strong free cash flow, and investors begin valuing them as strategic AI infrastructure suppliers rather than traditional commodity memory manufacturers.

Base Scenario

HBM grows rapidly, but pricing and margins gradually normalize as supply expands. SK Hynix remains the leader with some share dilution. Micron establishes itself as a credible second supplier and improves its product mix. Conventional memory remains cyclical, preventing either company from receiving a software-like valuation. Returns depend heavily on entry price and management's capital discipline.

Bear Scenario

AI spending growth slows, customer inventories rise, and new HBM capacity arrives into weaker demand. Pricing falls, qualification delays affect selected products, and conventional memory also softens. Earnings estimates decline rapidly. Stocks that looked inexpensive on peak earnings become expensive on normalized profits, and capital expenditure limits free cash flow.

The base scenario is the most reasonable starting point because it respects both structural demand and cyclical supply. The bull scenario is plausible, but investors should not make it their only case. The bear scenario does not require AI to fail. It requires only that expectations and supply run ahead of demand.

Which Stock Is Better for Different Types of Investors?

For investors prioritizing competitive quality: SK Hynix is the stronger choice. It has the clearest evidence of HBM leadership, high-volume execution, and customer trust.

For investors prioritizing accessibility and U.S. market structure: Micron is simpler. It trades directly on Nasdaq, reports through the SEC, and integrates easily into U.S. portfolios.

For investors seeking a share-gain catalyst: Micron has greater catch-up potential. The reward is higher if it closes the gap, but the thesis is more dependent on future execution.

For investors seeking the cleanest current HBM leader: SK Hynix offers the better operating exposure, although investors must evaluate the available security, currency, liquidity, and valuation.

For risk-averse investors: neither stock should be treated as low risk. Both operate in a capital-intensive semiconductor industry and are exposed to AI spending, memory pricing, technological transitions, and geopolitics.

For diversified investors: owning both can reduce company-specific qualification risk, but it does not eliminate industry risk. If HBM pricing collapses, both holdings can fall together.

What Smart Analysts Disagree About

The first disagreement is whether HBM has created a permanently better business. Bulls emphasize qualification barriers, long-term agreements, customization, and concentrated supply. Bears argue that capital intensity and competition will eventually restore commodity economics. Both sides have evidence. The resolution will appear in margins and free cash flow across a complete cycle, not during the strongest year.

The second disagreement is whether the leader or challenger offers better risk-adjusted returns. SK Hynix has stronger execution but higher embedded expectations. Micron has more room to improve but more ways to disappoint. Quality and upside are not the same concept.

The third disagreement concerns AI capital expenditure. One group believes spending is the foundation of a multi-year computing platform shift. Another believes customers are overbuilding before monetization is proven. The most likely outcome may contain both: a durable long-term trend interrupted by painful inventory and spending corrections.

The fourth disagreement is the role of custom accelerators. They may reduce Nvidia's share but expand the number of HBM customers. Alternatively, cost-optimized chips may use different memory mixes and weaken premium content. Investors should track system-level memory demand rather than use accelerator market share as a shortcut.

The fifth disagreement is valuation. Some analysts use near-term earnings and conclude the stocks are inexpensive. Others normalize margins and see peak-cycle risk. The difference usually comes from assumptions, not arithmetic.

What Would Change Our Verdict?

We would become more bullish on SK Hynix if it maintained clear leadership through HBM4 qualification, diversified its customer base, protected gross margins as competitors expanded, and converted record profits into sustained free cash flow after capital expenditure. Evidence that customized HBM creates longer contracts and stronger switching costs would further support a premium valuation.

We would become less bullish on SK Hynix if its share declined faster than the market expanded, if next-generation qualifications slipped, or if margins compressed despite strong demand. A rapid increase in capital expenditure without durable cash generation would also weaken the case.

We would become more bullish on Micron if HBM4 reached volume production on schedule, yields improved as expected, major customer allocations expanded, and HBM growth produced visible gross-margin and free-cash-flow gains. A broader customer base would reduce the risk that one qualification determines the story.

We would become less bullish on Micron if the catch-up remained confined to product claims rather than shipments, or if spending increased faster than qualified demand. A return to aggressive industry share competition would be especially concerning.

For both companies, the most important positive signal would be evidence that attractive returns survive after supply catches up. The most important negative signal would be weakening forward agreements, shorter lead times, rising customer inventories, and simultaneous price pressure across HBM and conventional DRAM.

Final Verdict: Leadership vs. Catch-Up

SK Hynix is currently the better company in HBM. Its market position, production experience, customer relationships, and financial results provide stronger evidence than a future roadmap alone. For investors who want the clearest exposure to current AI memory leadership, it deserves first consideration.

Micron may be the more interesting stock when valuation and catalyst are favorable. It does not need to overtake SK Hynix to create value. It needs to qualify competitive products, gain profitable allocations, improve mix, and avoid overspending into a future supply glut. If it accomplishes those goals, earnings expectations can rise rapidly.

The choice is therefore not simply “leader good, challenger bad.” SK Hynix carries lower relative execution risk but may carry higher expectations. Micron carries higher execution risk but offers more potential positive surprise. The better investment depends on the price paid and the probability an investor assigns to each scenario.

Our conclusion is:

Best current HBM business: SK Hynix.

Best U.S.-listed catch-up opportunity: Micron.

Biggest shared risk: investors assuming that today's scarcity and margins will last indefinitely.

Most important next evidence: HBM4 qualification, volume yields, customer allocation, industry capex, and free cash flow.

The AI memory boom is real, but a real boom can still produce overvaluation and overcapacity. Investors should avoid treating HBM as either a temporary fad or a cycle-proof miracle. It is a strategically valuable technology operating inside a capital-intensive industry. The winners will be the companies that combine technical execution with supply discipline, and the winning investors will be those who distinguish a durable advantage from expectations already priced for perfection.

Investor Checklist for the Next Two Earnings Cycles

Did HBM shipments and revenue grow at or above management's prior expectations?

Did gross margin improve after accounting for ramp costs?

Are HBM4 products qualified, shipping, and achieving mature yields?

Did the customer base broaden, or did concentration increase?

Are 2027 supply discussions supported by firm price and volume commitments?

How fast is industry packaging and wafer capacity expanding?

Are conventional DRAM and NAND inventories healthy?

Is free cash flow growing after capital expenditure?

Are hyperscalers raising or lowering AI infrastructure budgets?

Has valuation moved faster than normalized earnings power?

This checklist is more useful than reacting to a single price move. A stock can rise on excitement while its underlying risk increases, or fall while its long-term economics improve. The purpose of fundamental research is to identify which event occurred.

Frequently Asked Questions

Is SK Hynix the market leader in HBM?

SK Hynix entered 2026 as the clear HBM leader by commonly cited shipment and revenue estimates. Its early position in advanced HBM and relationships with leading accelerator customers support that status. Market share can change, however, and investors should track each new generation separately.

Can Micron catch SK Hynix?

Micron can gain meaningful share without becoming number one. Its opportunity depends on customer qualification, HBM4 execution, yields, and profitable volume. Customers have strategic reasons to diversify supply, but they will not sacrifice performance or reliability simply to create competition.

Does HBM eliminate the memory cycle?

No. HBM improves differentiation, visibility, and product value, but suppliers still invest in expensive capacity and remain exposed to demand changes. The cycle may become structurally better without disappearing.

Is Micron a pure AI stock?

No. AI and data centers are increasingly important, but Micron also sells memory and storage into other markets. Conventional DRAM, NAND, PCs, smartphones, autos, and industrial demand can affect its results.

Is SK Hynix a better buy than Micron?

SK Hynix has the stronger current HBM business, while Micron offers a more accessible U.S.-listed catch-up thesis. The better stock depends on valuation, investor risk tolerance, and confidence in future execution. Business quality alone does not determine investment return.

What is the biggest risk to both stocks?

The biggest shared risk is that capacity and expectations grow faster than end demand. AI can remain a major long-term trend while memory prices, margins, and stock valuations fall during a correction.

Sources and Further Reading

Disclosure: This article is for informational and educational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any security. Semiconductor markets are volatile, and investors should conduct independent research and consider their own objectives and risk tolerance.