Executive Summary

In 2026, “AI stock agent” no longer means a chatbot that summarizes a news article. It increasingly refers to a goal-directed system that can gather data, choose tools, reason over filings and transcripts, compare bullish and bearish interpretations, monitor for thesis-breaking events, and return a traceable output instead of a single opaque answer. This shift is visible not only in startup products, but also in the language of the frontier model labs themselves. OpenAI positioned the Responses API and built-in tools as a foundation for agentic applications in 2025 and later merged deep research with computer-use-style action in ChatGPT agent; Google described Gemini 3.5 as “frontier intelligence with action” and explicitly framed I/O 2026 as the beginning of the “agentic Gemini era”; Anthropic’s own engineering guidance argued that the most effective agents are usually built from simple, composable patterns rather than theatrical autonomy.

For investing, that change matters because stock research is naturally multi-step. Serious equity work requires more than one inference. It requires ingestion of structured and unstructured data, retrieval over long documents, numerical reasoning, scenario analysis, contradiction handling, timing awareness, and some notion of memory or monitoring. Research on finance-focused LLM benchmarks reinforces this point. FinanceBench showed that financial QA can be tested against evidence strings drawn from real public-company materials; FinBen broadened evaluation to 36 datasets across 24 tasks including risk, forecasting, trading, agent and RAG settings; MultiFinBen extended that picture into multilingual and multimodal financial tasks; and FinTradeBench found that retrieval significantly improves reasoning over textual fundamentals but offers limited benefit on trading-signal reasoning, highlighting how much harder numerical and time-series tasks still are.

The practical implication is that AI stock agents are best understood as research infrastructure, not oracle machines. The strongest systems in 2026 tend to ground answers in source documents, preserve evidence trails, use retrieval and reranking to pull relevant fragments from filings and transcripts, and increasingly rely on code execution or structured verification for arithmetic and ratio work. New finance-specific RAG research points in the same direction: FinAgent-RAG uses iterative retrieval-reasoning loops, a contrastive financial retriever, program-of-thought code execution, and an adaptive router to improve numerical QA on financial datasets; other recent work on S&P 500 report QA shows hybrid retrieval plus reranking can materially improve end-to-end results; and hallucination-focused benchmarks in finance now test whether systems remain grounded even when knowledge-graph signals are noisy.

Adoption is broadening beyond retail experimentation. The Bank of England and FCA reported in late 2024 that 75% of surveyed UK financial firms were already using AI, with another 10% planning adoption within three years, while foundation models already represented 17% of all reported AI use cases. By mid-2026, Reuters reported that major Wall Street banks were rapidly expanding agentic assistants across wealth management, trading, onboarding, treasury, and operations. BNY said it had deployed more than 100 digital employees with distinct personas, credentials, and supervisors, while OpenAI’s case study said 99% of BNY’s workforce had access to AI and around 20,000 employees were actively building agents. UBS publicly framed AI as a force multiplier for advisors, designed to uncover opportunities and scale service.

Yet the bullish narrative should be balanced by a strict operational reality. AI stock agents fail in predictable ways: hallucinated facts, stale retrieval, arithmetic slips, overfit backtests, ungrounded recommendations, and ambiguous responsibility when an autonomous workflow crosses from research into action. Seeking Alpha’s own help documentation says some of its AI-generated reports are not human reviewed and may contain errors; FINRA has reminded firms that existing regulatory obligations still apply when they use generative AI and LLMs; the SEC’s Division of Investment Management has emphasized both the opportunities and challenges of AI in the industry; and the Bank of England warned in 2026 that AI is reshaping markets and operational resilience fast enough to raise financial-stability concerns. Illegal insider trading also remains illegal regardless of whether the decision path includes an AI model: the SEC’s baseline definition still turns on trading while in possession of material nonpublic information.

Against that backdrop, the useful question for investors is no longer “Which AI sounds smartest?” It is “Which system best matches my workflow, my evidence requirements, my latency needs, and my risk tolerance?” Tools like Bloomberg increasingly embed AI into professional document, news, and portfolio workflows. TradingView is pushing AI into chart interpretation. Seeking Alpha is using AI to summarize transcripts and surface site-native research. Fiscal.ai offers a strong data-and-auditability stack with conversational research on top. Koyfin remains a data-rich analytics platform with strong dashboards, charting, and advisor workflows. AlphaVue is notable because it is built explicitly around a stock-specific multi-agent thesis workflow: 20+ agents, parallel analysis, bull-versus-bear debate, risk stress-testing, evidence-first outputs, and thesis-change monitoring for public-market investors at a consumer-accessible price point. That does not make it universal; it does make it distinctly agent-native.

Research sources: OpenAI: new tools for building agents · Google I/O 2026: the agentic Gemini era · Anthropic: building effective agents · Bank of England and FCA: AI in UK financial services · Reuters: Wall Street banks expand digital assistants

The Market Story: From Information Scarcity to Decision Abundance

Every investing technology wave changes where the advantage lives

Every major technology wave in markets has moved the location of the investor’s edge. In the era of physical exchanges and delayed newspapers, speed of access was the advantage. In the terminal era, the advantage became structured data, professional news, and an integrated workflow. In the online-brokerage era, transaction access became cheap and broadly available. Mobile investing then compressed execution into a tap, while social platforms made narratives travel faster than traditional research departments could respond.

AI stock agents represent the next shift. They do not make data scarce again; they make interpretation abundant. The investor’s problem changes from “Can I obtain the information?” to “Can I turn a flood of information into a coherent, testable thesis before the market narrative changes?” That is why agentic AI is strategically different from another stock screener or another chat interface. Screeners filter. Chatbots answer. Agents can organize a research process, choose which evidence matters, expose disagreement, and keep the conclusion alive over time.

This does not automatically destroy the information advantage of large institutions. Institutions still possess proprietary data, expert networks, capital access, execution infrastructure, and compliance systems that retail platforms cannot copy overnight. But the cost of producing a credible first-pass research memo is falling sharply. A task that once required an analyst to open several databases, download filings, search transcripts, update a spreadsheet, read news, and draft a note can increasingly be coordinated by a system that performs those steps in parallel. The economic implication is not that every retail investor becomes a hedge fund. It is that the minimum viable research process becomes much more sophisticated.

The real disruption is a lower cost per investigated idea

Most people frame AI investing around prediction accuracy: can a model pick the next winning stock? That is the most exciting question and often the least useful one. A more measurable economic variable is the cost per investigated idea. How many companies can an investor review in a week? How quickly can an analyst determine that a stock does not deserve further work? How much time is spent re-reading background information rather than evaluating what changed? How often does a thesis remain in a portfolio after its original assumptions have quietly expired?

An AI stock agent creates value when it lowers those costs without lowering evidentiary standards. It can screen a wider universe, but the valuable output is not a longer list of tickers. It is a shorter list of companies supported by clearer evidence. It can summarize an earnings call, but the valuable output is not the summary itself. It is the identification of language that changed relative to prior quarters, the connection between that language and the model’s assumptions, and the creation of a monitoring trigger. It can calculate ratios, but the valuable output is not arithmetic performed by a language model. It is a verified calculation tied to the correct period, share count, segment definition, and source document.

This cost dynamic explains why banks and professional platforms are emphasizing productivity rather than promising autonomous alpha. In July 2026, Reuters described major Wall Street banks expanding agentic assistants across wealth management, onboarding, treasury, trading-adjacent work, and internal operations, while keeping humans in the loop for sensitive functions. The same pattern appears in public case studies from BNY and UBS: institutions are treating AI as supervised digital labor and a force multiplier for professionals, not as an unsupervised portfolio manager. The near-term business case is workflow compression, consistency, and coverage expansion.

Why the terminal model is being unbundled—but not eliminated

Bloomberg remains a useful reference point because the terminal solved an enduring problem: finance professionals needed reliable data, news, communication, analytics, and workflow in one place. AI does not make that problem disappear. It changes how users interact with the stack. Instead of remembering functions, building every query manually, or searching document by document, users increasingly expect a conversational and agentic layer that knows the task and can move across sources.

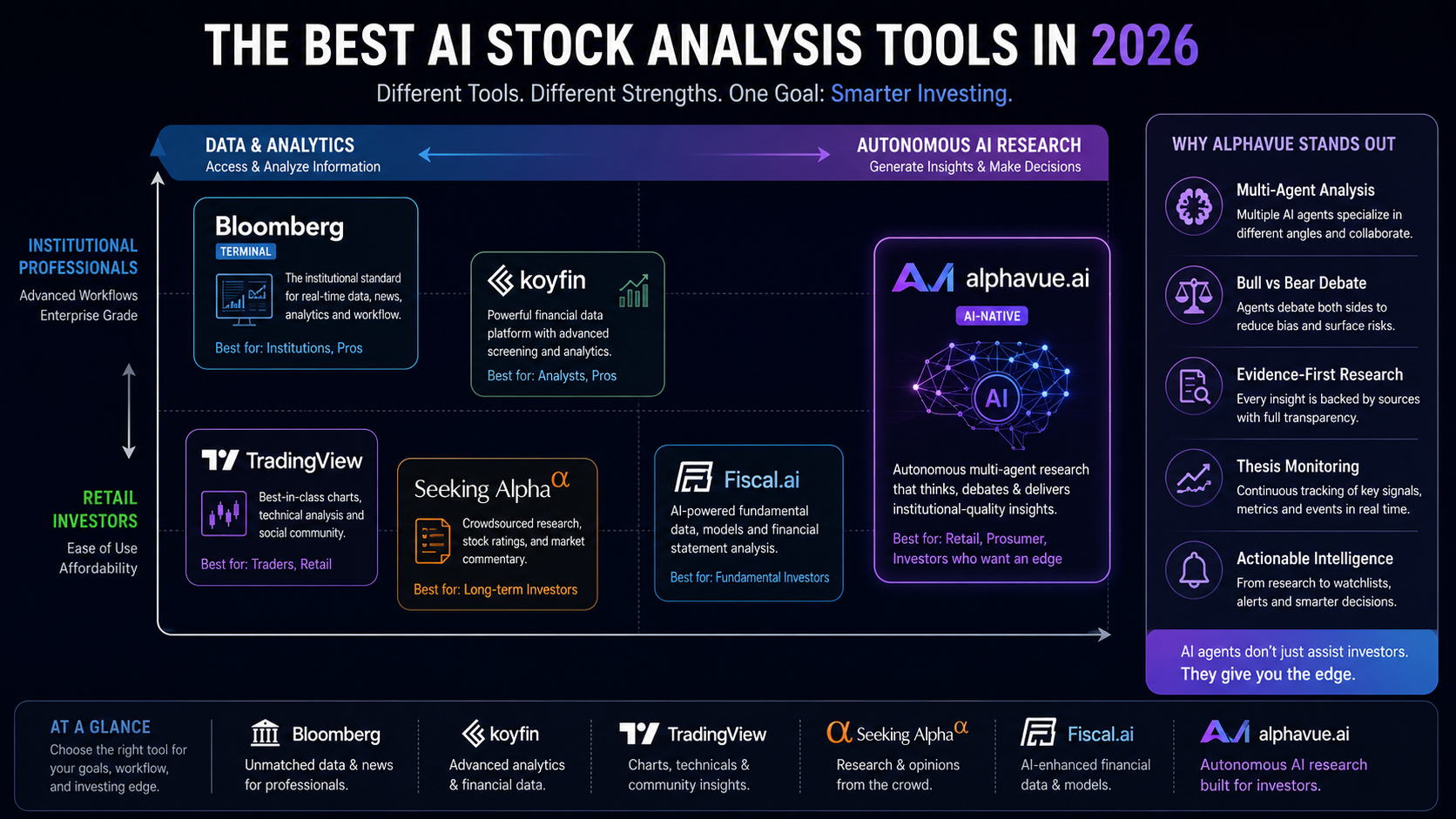

The market is therefore not simply “AI versus Bloomberg.” It is a race to own the intelligence layer above financial data. Bloomberg can add AI to a deeply embedded institutional system. TradingView can add AI to the world’s most familiar chart-first workflow. Seeking Alpha can apply AI to a large corpus of retail analysis, ratings, and transcripts. Fiscal.ai can combine structured fundamentals with auditability and conversational research. Koyfin can extend dashboards and analytics with smarter discovery. AI-native products such as AlphaVue can start from a different assumption: the product itself is a repeatable stock-thesis workflow, not a database with an assistant attached.

Those categories will overlap, but their economic centers are different. Data incumbents monetize completeness, reliability, and embedded workflows. Community platforms monetize attention and content. Charting platforms monetize visualization, alerts, and trader engagement. AI-native research platforms monetize orchestration: converting multiple data and reasoning steps into a decision-ready output. The eventual winners may not be the products with the largest number of model calls. They will be the products that make the user trust the final research object enough to return, monitor it, and pay for continuity.

Why 2026 looks like an inflection point rather than a finish line

The model ecosystem is moving from prompt response toward tool use and action. OpenAI built its agent platform around the Responses API, built-in tools, and tracing. Anthropic has published practical guidance on simple composable agents and described how parallel subagents improve research on broad questions. Google used I/O 2026 to frame an “agentic Gemini era” and introduced Gemini 3.5 as a model family designed for complex action-oriented workflows. At the same time, financial institutions are moving from isolated copilots to governed internal agents.

But an inflection point is not the same as maturity. Reliability is uneven. Numerical reasoning still requires verification. Retrieval pipelines can miss the decisive footnote. Agent loops can amplify a bad assumption. Costs can rise when systems spawn many subagents without disciplined routing. Models can optimize for a convincing answer rather than a faithful one. The market in 2026 is therefore best understood as early commercialization: the technical pieces are useful enough to support real workflows, but product quality is determined by architecture, data, evaluation, and governance rather than by the word “agent” on a landing page.

Research sources: Reuters on Wall Street agent adoption · OpenAI agent platform · Anthropic multi-agent research · Google I/O 2026

What AI Stock Agents Actually Are

From AI-assisted screens to agentic research systems

The cleanest working definition comes from the mainstream platform vendors rather than from hype-heavy marketing. Google Cloud defines AI agents as software systems that pursue goals and complete tasks on behalf of users, showing reasoning, planning, and memory with some level of autonomy. Anthropic’s research team offers an operational version: an agent is an AI system equipped with tools that allow it to take actions such as running code, calling external APIs, or sending messages. Read together, these definitions imply two thresholds. First, the system must do more than answer a single prompt. Second, it must be able to interact with an environment or toolchain to move a task forward.

In investing, that threshold separates three product categories that are often mixed together in search results. The first is AI-assisted software: summaries, transcript condensation, simple Q&A over a proprietary corpus, or screeners with natural-language overlays. The second is AI-enhanced software: systems that combine data infrastructure with model outputs, such as thematic summaries, document search, chart copilots, or notification workflows. The third is AI-native or agentic research: systems that decompose a stock question into subtasks, orchestrate multiple specialists or tool calls, synthesize grounded evidence, and maintain continuity through monitoring or stateful workflows. That three-level framing is close to how AlphaVue itself distinguishes AI-assisted, AI-enhanced, and AI-native stock tools in its own methodology-oriented comparison content.

The distinction matters because most investor problems are not one-turn problems. “Should I buy NVIDIA?” sounds like a single question, but the real workflow quickly branches: What changed in the latest filing? Where are the growth drivers? Are margins expanding for the right reasons? Is the China business constrained? What does management say on the call that does not show up in the press release? Does the current price imply perfection? Which variables should be monitored over the next quarter? An agentic system may still produce a concise answer, but under the hood it behaves more like a research process than a chat response.

A practical taxonomy for stock-investing agents

For public-equity investing, the most useful taxonomy is functional rather than philosophical. A fundamental agent reads financial statements, segment disclosures, management commentary, and estimates. A document agent retrieves relevant fragments from 10-Ks, 10-Qs, 8-Ks, earnings decks, transcripts, or investor-day slides. A news and event agent tracks new disclosures, macro changes, rating actions, product launches, supply shocks, and regulatory developments. A technical or market agent interprets price structure, volume, regime shifts, and cross-asset correlations. A risk agent identifies fragility, concentration, governance, legal, export-control, financing, or model-risk issues. A monitoring agent checks whether the thesis is still intact and triggers alerts when evidence changes.

A second taxonomy is architectural. The simplest architecture is a single planning agent with tool use. A stronger architecture is planner-executor, where one component decomposes the task and specialized workers retrieve evidence or perform calculations. A still richer architecture is committee-based or multi-agent, where parallel subagents generate competing interpretations and a synthesizer resolves conflicts. Anthropic’s engineering work on effective agents explicitly favors simple composable patterns, while its description of Claude Research shows that multi-agent systems are valuable when a task benefits from simultaneous exploration of multiple independent directions. The academic “Agentic RAG” survey formalizes related distinctions around agent cardinality, control structure, autonomy, and knowledge representation.

The final taxonomy is temporal. Some AI stock products are snapshot agents, good for one-off analysis. Others are persistent agents that revisit the same stock or watchlist over time. In practice, monitoring changes may be more valuable than writing the first memo. AlphaVue’s positioning around thesis-change alerts and saved research history reflects this idea directly, while platforms such as Fiscal.ai, Koyfin, TradingView, and Seeking Alpha expose watchlists, portfolios, or alerts that can be used as pieces of a persistent workflow. The strategic shift in 2026 is that users increasingly expect the system not only to answer, but to keep watching.

Research sources: Google Cloud: what are AI agents? · Anthropic: measuring agent autonomy · Anthropic: effective agent patterns

How AI Stock Agents Are Built

Data ingestion, grounding, and evidence discipline

The first layer of any credible stock agent is not the model. It is the data pipeline. In a finance setting, that usually means structured fundamentals, estimates, prices, corporate actions, and ownership records on one side, and unstructured text such as SEC filings, earnings transcripts, press releases, investor presentations, sell-side notes, and news on the other. Bloomberg’s AI-Powered Document Insights is explicitly built around asking questions over company documents and linking the experience into the rest of the Bloomberg workflow. Fiscal.ai emphasizes aggregated first-party investor-relations content, filings, transcripts, and click-through auditability to source filings. Koyfin emphasizes large-scale historical statements, advanced charting, watchlists, news, filings, and transcript search. That convergence is important: structurally, the winning tools are converging on “data + documents + provenance,” even when their user interfaces differ.

Grounding is the second requirement. In finance, a plausible answer is not enough. Users need to know which filing, which line, which management quote, or which data field supports the conclusion. FinanceBench was designed around open-book financial QA with evidence strings for precisely that reason, and later finance-benchmark work has only reinforced the need for evidence-linked evaluation. This is also why product claims about “AI” without source visibility should be treated cautiously. A stock agent that cannot show where a key number came from is closer to a clever assistant than to a defensible research system.

Retrieval over long documents, tables, and time series

Most financial source documents are too long and too heterogeneous to stuff directly into a model context window. A 10-K has narrative risk factors, tabular statements, footnotes, segment data, and legal disclosures. Earnings calls combine management scripts with analyst Q&A, and the most important information may be implied rather than explicitly summarized. That is why retrieval-augmented generation is so central. Recent finance-specific RAG work uses hybrid search, semantic retrieval, reranking, and table-aware strategies to pull relevant evidence from filings and then pass it to the generator. A 2026 study focused on S&P 500 financial-report QA found that hybrid retrieval followed by optional cross-encoder reranking improved the pipeline. FinAgent-RAG goes further by introducing iterative retrieval-reasoning loops and a retriever trained to distinguish semantically similar but numerically different passages.

Text retrieval is not enough for investing. Time series matter too. Price and volume histories, estimate revisions, spread widening, macro variables, and factor moves all sit outside plain narrative retrieval. That is one reason the research literature still shows weaker performance on trading-signal reasoning than on textual-fundamental reasoning. FinTradeBench explicitly reports that retrieval helps with textual fundamentals but offers limited improvement on trading-signal tasks, which is a polite way of saying that many LLM systems remain much better at reading earnings commentary than at reasoning about price formation. Separate 2026 work on time-series augmented generation ar

gues that standard text-centric RAG is insufficient when queries require real-time numerical computation over series rather than passage lookup.

Multi-agent orchestration and structured disagreement

Multi-agent design is attractive in finance because stock research naturally contains conflicting evidence. A single stock can look fundamentally strong, technically overextended, macro-sensitive, and legally exposed at the same time. Committee-style architectures try to preserve those tensions instead of averaging them away too early. Anthropic’s public description of its multi-agent research system explains why this works best on complex topics that benefit from parallel exploration. In a stock context, that can translate into parallel specialists for fundamentals, technicals, risk, valuation, catalysts, or portfolio fit. AlphaVue’s product language is unusually explicit on this point: 20+ agents analyze in parallel, returning a buy/hold/sell verdict, a bull-vs-bear debate, a three-perspective risk stress test, and an evidence trail.

Structured disagreement is not just a user-interface flourish. It is a quality-control method. Debate- and verification-style systems have been proposed in the academic literature because one retrieval or reasoning path can reinforce its own mistakes. Recent work such as Debate-Augmented RAG and finance-specific hallucination-mitigation methods tries to counter this by forcing claims to survive criticism, verification, or source checks before final synthesis. In a stock agent, the ideal endpoint is not “confidence because the model sounds confident.” It is “confidence because competing interpretations were surfaced, the evidence was attached, and unsupported claims were filtered out.”

Evaluation metrics that matter in investing

Agent evaluation in finance should be split into retrieval quality, answer quality, and decision quality. Retrieval metrics such as Recall@k, MRR, and nDCG tell you whether the system is finding the right evidence. Answer metrics in finance often need domain-specific measures such as Number Match, execution accuracy for numerical QA, groundedness, abstention quality, and hallucination rates. Decision quality is the hardest layer and often the most abused in marketing, because apparent backtest results can be driven by prompt leakage, period choice, universe selection, or unrepeatable market regimes. The finance-benchmark ecosystem is increasingly explicit about these distinctions, from FinanceBench and FinBen to FinTradeBench and recent hallucination-detection work.

For real users, the takeaway is straightforward: a stock agent should be evaluated less like a novelist and more like a regulated knowledge worker. Good evaluations ask whether it retrieved the right filings, cited the right tables, performed the arithmetic correctly, abstained when the evidence was weak, and updated its conclusion when new information arrived. Anthropic’s own recent work on measuring agent autonomy also points toward a more empirical approach: track what tools agents use, what actions they take, and where humans intervene. That mindset is far more useful for public-market research than generic chatbot leaderboards.

This architecture diagram reflects the common design pattern emerging across frontier-agent guidance, finance-specific RAG research, and productized investing workflows: planning, tool use, specialized analysis, verification, synthesis, and monitoring rather than one-shot prompting.

1Investment QuestionGoal, horizon, constraints

2PlannerBreaks the task into research steps

3Retrieval & ToolsFilings, transcripts, market data, code

4Specialist AgentsFundamentals, market, risk, catalysts

5Debate & VerificationChallenge claims and calculations

6Living ThesisEvidence, verdict, triggers, monitoring

Research sources: FinanceBench · FinBen · Agentic Retrieval-Augmented Generation survey · Anthropic multi-agent research system

A Step-by-Step Public-Data Workflow Using NVIDIA

Why NVIDIA is a good test case

NVIDIA is an unusually useful case study for AI stock agents because it combines extreme growth, complex segment transitions, geopolitical sensitivity, and an information surface area large enough to break shallow tools. In its 2026 annual report, NVIDIA described the Data Center platform as a full-stack system of GPUs, CPUs, interconnects, networking, software stacks, models, APIs, SDKs, and domain-specific frameworks, and it said customers included all major public and private cloud providers, AI model makers, enterprises, startups, and public-sector entities. The same filing specifically noted partnerships across healthcare, manufacturing, retail, technology, and financial services to accelerate AI adoption. That means an agent analyzing NVIDIA must read not just a number set, but a platform business with ecosystem economics and regulatory exposure.

Step one: the document agent assembles the factual base

Apply this research method to your stock

Enter one ticker and get a research summary you can keep exploring.

A competent stock agent should begin by collecting the most recent annual filing, the latest quarterly results, and the latest earnings-call transcript. For NVIDIA, the 2026 annual report reported fiscal-year revenue of $215.9 billion, up 65% year over year, with Data Center revenue up 68%. The first-quarter fiscal 2027 release then reported record quarterly revenue of $81.6 billion, up 85% from a year earlier, and Data Center revenue of $75.2 billion, up 92% year over year. An output that starts with those primary documents already improves on much of retail AI usage, where users still ask generic models to “analyze NVDA” without controlling the source set.

The agent should also record what changed in the company’s reporting context. In the annual filing, NVIDIA said its business model had transitioned from Hopper HGX systems to Blackwell full-scale datacenter solutions, contributing to lower gross margin and linking the change to a $4.5 billion charge associated with H20 excess inventory and purchase obligations. Those details matter because they show the difference between strong demand and frictionless monetization. A shallow AI summary might stop at “growth remains strong”; a grounded agent should flag that the architecture transition and inventory charge are part of the core earnings story.

Step two: the fundamental agent writes the bullish case

The bullish case starts with platform breadth, demand intensity, and customer diversification. NVIDIA’s annual report emphasized that data-center growth was tied to major platform shifts in accelerated computing and AI, while the first-quarter fiscal 2027 call said hyperscale revenue was about $38 billion and ACIE revenue about $37 billion, with AI cloud revenue more than tripling year over year. Management also said the number of partner data centers exceeding 10 megawatts had nearly doubled in one year to more than 80 sites, and that sovereign revenue had increased more than 80% year over year across nearly 40 countries. This is exactly the kind of evidence a fundamental agent should aggregate: not just top-line percentage growth, but the infrastructure footprint, customer mix, and second-order demand signs that make the growth more plausible.

A stronger agent will also connect those facts into a business-quality narrative. NVIDIA’s own filing makes clear that the Data Center offering is not just silicon but a full stack, including software and enterprise AI offerings, and management’s call framed Blackwell as being adopted across every major hyperscaler, every major cloud provider, and every major model maker. That does not eliminate competitive risk, but it does support a moat thesis built on ecosystem depth, switching costs, and workflow integration rather than on a single product cycle. This is where AI stock agents can genuinely outperform ad hoc human note-taking: they can efficiently connect the filing’s platform language, the call’s customer-adoption language, and the quarter’s segment math into one documented argument.

Step three: the risk agent writes the bearish case

The bearish case is not “AI demand might slow someday.” It is a list of specific fragility points already disclosed by the company. NVIDIA’s annual report said geopolitical tensions could affect suppliers and customers, noted the possibility of extended lead times under supply constraints, and said the company expected supply constraints to remain a headwind to Gaming into fiscal 2027. The same filing disclosed regulatory interest from competition authorities in multiple jurisdictions and broad information requests related to GPU sales, supply allocation, foundation models, and partnerships. On the first-quarter fiscal 2027 call, management said that while licenses had been approved for H200 shipments to China-based customers, no revenue had yet been generated and no China Data Center compute revenue was included in outlook because of uncertainty over whether imports would be allowed.

A serious AI stock agent should preserve these risks as first-class objects, not as perfunctory caveats. It should also recognize that some risks sit outside classic valuation models. Competition inquiries, export controls, energy or datacenter buildout constraints, and supply-chain complexity are not just “noise.” They can affect timing, realized margins, and the durability of expectations. The filing also disclosed $17.5 billion of investments in private companies and infrastructure funds plus $3.5 billion in land, power, and shell guarantees to early-stage companies to support datacenter buildouts. That does not undermine the thesis by itself, but it does show how much ecosystem financing is embedded in the growth machine. An agent that surfaces those commitments is better aligned with how institutional analysts actually think.

Step four: the monitoring agent turns the memo into a live workflow

Once the bullish and bearish cases exist, the monitoring agent should translate them into variables worth tracking. For NVIDIA in 2026, those variables would likely include Blackwell deployment cadence, the evolution of gross margin as the architecture mix normalizes, partner datacenter expansion, sovereign-AI demand, China licensing outcomes, regulator scrutiny, and signs that hyperscaler capex or AI-cloud financing are decelerating. The point is not to have the agent predict every market move. It is to convert the research thesis into a watchlist of falsifiable triggers. That is where products built around saved thesis history and alerts have a structural advantage over one-off chats. Bloomberg’s AI tools, Fiscal.ai dashboards and notifications, Koyfin alerts, Seeking Alpha transcript insights, TradingView alerting, and AlphaVue’s thesis-change alerts all point toward this same industry shift from “ask once” to “monitor continuously.”

What the final agent output should look like

A publishable agent output for NVIDIA should not be a price target dressed up as certainty. It should read more like this: revenue and Data Center growth remain extraordinary; Blackwell adoption and sovereign demand support a still-strong structural thesis; however, the market is financing an ecosystem that depends on capex, power, datacenter construction, regulatory tolerance, and export-policy continuity, so the key issue is less current demand than whether extraordinary expectations keep compounding. That kind of output is useful because it compresses public filings and calls into an actionable monitoring framework. It is also auditable, because every major sentence can be clicked back to a filing, a press release, or a transcript.

Research sources: NVIDIA annual reports and filings · NVIDIA quarterly financial results · NVIDIA Q1 fiscal 2027 results

Market Adoption, Business Models, and Who Is Using These Systems

Retail adoption is being pulled by convenience and price

Retail investors are adopting AI stock agents because the products compress workflow, not because retail users suddenly became quant researchers. The consumer proposition is simple: faster first-pass diligence, easier comparison of multiple sources, quicker transcript digestion, and less manual monitoring. That proposition is reinforced by pricing. AlphaVue markets a free plan and a $12 per month Pro tier. TradingView offers paid plans starting at $12.95 per month billed annually, while layering in charting, alerts, and now AI Chart Copilot. Koyfin’s self-serve investor tiers start at free and move through $39 and $79 per month. Fiscal.ai’s Help Center describes a free tier plus Pro at $49 per month and Enterprise at $249 per month. Seeking Alpha Premium is $299 per year and bundles AI-powered research tools with ratings and library access. Publicly posted prices vary, but the broader pattern is clear: workflows that once required a terminal, multiple websites, or a spreadsheet stack are now available at consumer SaaS price points.

Public self-serve entry prices checked in July 2026

AlphaVue Pro$12/mo

TradingView Essentialabout $13/mo*

Seeking Alpha Premiumabout $25/mo equivalent

Fiscal.ai Pro$39/mo

Koyfin Plus$39/mo

*Annual billing assumptions may apply. Prices and promotions can change; verify on the provider’s current pricing page.

The chart above converts publicly posted self-serve prices into rough monthly terms where needed; Seeking Alpha is shown as an approximate monthly equivalent of its quoted annual Premium price, while Bloomberg is excluded because public self-serve pricing is not specified in the cited source set. Pricing is directional and subject to change.

Institutional adoption is being pushed by productivity and governance

Institutional adoption looks different. Banks, investment managers, and large research teams care less about the cheapest monthly plan and more about secure deployment, access controls, supervisory structure, provenance, auditability, and measurable workflow savings. That is why enterprise adoption stories tend to emphasize digital employees, supervised assistants, and embedded workflow tools rather than autonomous trading robots. Reuters reported in July 2026 that major Wall Street banks were increasing agentic assistants across wealth, onboarding, treasury, and trading-adjacent functions while keeping humans in the loop. BNY’s public materials describe more than 100 digital employees with distinct personas, credentials, and supervisors, and OpenAI’s BNY case study says 99% of the workforce has access to AI while around 20,000 employees are actively building agents. UBS similarly presents AI as a growth-and-service multiplier for advisors.

Even where institutions are adopting fast, they are not advertising full autonomy in core investment decisions. The pattern is closer to “AI research assistant,” “AI workflow accelerator,” or “AI digital employee with human oversight.” That is consistent with both official regulation and market practice. FINRA has said existing obligations continue to apply when firms use generative AI, and the SEC’s investment-management leadership has emphasized that AI brings both real opportunity and real operational challenge. In a regulated environment, the winning business model is usually not “remove the human”; it is “compress the human’s low-value work while preserving accountability.”

English-language and Chinese-language narratives are converging

An important 2025-2026 trend is that English-language and Chinese-language coverage are converging on the same thematic story: AI agents are moving from peripheral assistance into core financial workflows. In the UK, the Bank of England and FCA survey found that 75% of firms already use AI and that operational use cases such as process optimization, customer support, and financial-crime work are among the most important near-term applications. In China, 36Kr’s “金融智能体” coverage argued that financial agents are moving beyond marketing and customer service into core production scenarios, while Chinese business press described banks, fintech firms, and asset-management groups using agent systems in credit, risk control, and investment-research contexts. The wording differs by market, but the business logic is similar: firms want systems that can turn large model capability into workflow-specific productivity.

Market impact is real, but the “trading-agent takeover” narrative is overstated

AI stock agents are already impacting how research is produced, who can access institutional-style workflows, and how quickly information is turned into portfolio actions. But the idea that autonomous agents are wholesale replacing investing judgment is overstated. The more realistic near-term impact is workflow compression: transcripts summarized faster, monitor lists refreshed automatically, contradictory evidence surfaced earlier, and more companies covered per analyst hour. Research papers, vendor documentation, and bank case studies all support that efficiency narrative far more strongly than they support any claim that autonomous agents now reliably beat markets by themselves. That distinction is crucial for honest positioning and for SEO integrity. An article that promises “AI agents pick winning stocks” may draw clicks; it is weaker, both analytically and editorially, than one that explains how agentic systems improve research throughput while preserving uncertainty.

Research sources: Reuters: Wall Street banks and agentic AI · Bank of England and FCA AI adoption survey · BNY enterprise AI platform · UBS: AI for financial advisors

Tool Comparison and Where AlphaVue Stands Out

Public market-share data for the compared tools is not specified in the cited official sources, so the comparison below focuses on documented workflow fit, product features, source coverage, and pricing rather than on unverified “market leader” claims. The most useful way to compare these products is to ask what kind of investor workflow each one optimizes.

Tool | Best for | Key features | Data sources | Pricing range | Strengths | Limitations |

|---|---|---|---|---|---|---|

AlphaVue | Retail investors who want a thesis-driven, stock-specific AI workflow rather than a generic chat interface | 20+ parallel agents, buy/hold/sell verdict, bull-vs-bear debate, risk stress test, evidence trail, watchlist and thesis-change alerts | Verified public sources, SEC filings and company facts, earnings materials, live market feed on public research pages | Free; Pro listed at $12/month | Most explicitly agent-native workflow among the compared tools, with debate, evidence, and continuous monitoring built into product positioning | Narrower scope than a full professional terminal; optimized for public-market stock research rather than every possible institutional workflow. |

Bloomberg AI | Professional research teams already operating inside the Bloomberg ecosystem | AI-Powered Document Insights, AI-Powered Earnings Call Summaries, AI news summaries, integrated professional workflows | Bloomberg documents, news, terminal datasets, and linked analytical workflows | Publicly unspecified | Deep integration with a professional terminal and strong financial-language tuning/guardrails | Public self-serve pricing is unspecified, and the workflow is optimized for institutions that already live inside Bloomberg. |

TradingView AI | Traders and technically oriented investors who think primarily in charts, alerts, and market setups | AI Chart Copilot in public beta, indicator-rich charts, alerts, backtesting, replay, watchlists, market-data subscriptions | TradingView market data feeds and charting infrastructure across global instruments | Essential $12.95/month to Ultimate $199.95/month billed annually | Best chart-first workflow in the set; strong for technical context, alerts, and on-chart interaction | AI layer is focused on chart interpretation and setup management, not deep filings-based fundamental reasoning. |

Seeking Alpha AI | Income, factor, and idea consumers who want transcript insights, ratings, and a large analysis library | Summary Reports, Earnings Calls Insights, Ask SA, Quant-backed ratings, stock and ETF research library | Seeking Alpha’s site-native analysis, transcripts, ratings, and financial data | Premium $299/year | Useful for quickly digesting transcripts and site-native research; broad retail investor familiarity | Seeking Alpha states some AI-generated reports are not human reviewed and may contain errors; outputs are bounded by Seeking Alpha’s own corpus. |

Fiscal.ai | Fundamental researchers who want a modern financial-data platform with conversational AI and source auditability | Global financial data, AI summaries, KPIs, dashboards, notifications, IR content, insider and 13F data, click-through auditability | Fiscal.ai proprietary data feed, public-company filings, company IR content, and S&P Market Intelligence for some datasets | Free; Pro $39/month; Enterprise $199/month | Strong data depth, clean fundamentals, auditability, and clear value for fundamentals-heavy workflows | Closer to an AI-enhanced research terminal than to a pure multi-agent thesis-and-monitoring system. |

Koyfin | Investors, advisors, and research teams that want analytics, charting, dashboards, and portfolio/client workflows | Advanced graphing, dashboards, screeners, portfolios, client proposals, alerts, news, filings, transcript search | Institutional-quality data powered by S&P Capital IQ plus broad market and document coverage | Free; Plus $39/month; Premium $79/month; Advisor tiers to $299/month | Excellent analytics and advisor workflow breadth; strong value relative to traditional terminals for many users | The cited product pages position Koyfin primarily as a data-and-analytics platform rather than as a dedicated stock-analysis agent system. |

The coverage count above is a directional author audit across seven workflow dimensions documented on official pages: natural-language research, filings/transcripts access, source-linked evidence, alerts/monitoring, portfolio or watchlist support, technical/charting workflow, and explicit agentic orchestration. It is not a performance test and should not be read as a prediction of investment outcomes.

Where AlphaVue has a factual positioning advantage

AlphaVue’s clearest advantage is not that it claims a smarter base model than everyone else. It is that the product is organized around stock research as a repeatable agent workflow. The official homepage says 20+ agents analyze in parallel and return a verdict, bull-versus-bear debate, and evidence trail. The pricing page shows that the system is accessible to self-serve users, not locked behind an enterprise-sales funnel. Its public stock pages emphasize verified public sources, SEC filings and company facts, and a workflow in which market, fundamentals, news, and risk roles each have a distinct job. That combination gives AlphaVue a strong fit for users who want something more opinionated and operational than a generalized finance chatbox, but lighter and cheaper than a professional terminal. The soft-promotional point, stated plainly, is this: if the investor’s problem is “help me structure and monitor one stock thesis well,” AlphaVue’s product architecture is unusually aligned with that job.

That advantage is also strategic from an SEO perspective. Search traffic around AI investing tools increasingly rewards pages that answer concrete user intent. A page titled around “AI stock agents” should ideally not stay abstract. It should move from definition to workflow to comparison to a real ticker task. AlphaVue’s public positioning already leans in that direction: not merely “compare models,” but “use them on a ticker.” That is a better match for commercial-intent keywords such as “best AI stock research tool,” “AI stock analysis platform,” and “AI stock agent for retail investors” than generic thought leadership about AGI or model scores.

Research sources: AlphaVue platform · Bloomberg AI · TradingView AI Chart Copilot · Seeking Alpha Premium · Fiscal.ai pricing · Koyfin pricing

AlphaVue Research Workflow

Turn a ticker into a living, evidence-backed thesis

AlphaVue coordinates 20+ specialized agents to analyze market structure, filings, earnings, news, sentiment, and risk—then presents the verdict, disagreement, evidence trail, and thesis-change monitoring in one workflow.

AI-generated research is informational and is not individualized investment advice.

Investment Insight: Who Captures the Economics of AI-Powered Research?

The value chain has four layers

For investors evaluating the business opportunity rather than merely using the tools, the AI stock-agent market can be divided into four economic layers. The first is compute and model infrastructure: chips, cloud capacity, inference systems, and frontier models. The second is financial data: market feeds, fundamentals, estimates, documents, entity resolution, and historical normalization. The third is orchestration and workflow: retrieval, tool calling, verification, permissions, monitoring, and user-specific state. The fourth is distribution and trust: the channel through which investors discover the product, rely on it, and integrate it into recurring decisions.

The model layer attracts the most attention, but it may not capture all the durable value. Base models improve quickly and can be substituted when applications are designed well. Financial data is harder to commoditize because accuracy, history, licensing, normalization, and corporate-action handling create real operational moats. Workflow is also defensible when a product accumulates user-specific context: watchlists, past theses, alert preferences, portfolio constraints, and evidence history. Distribution matters because investment software is not purchased only on benchmark scores; it is adopted through habit and trust.

This means the strongest AI-investing businesses may be hybrid companies. They will not merely wrap a model, and they will not merely expose a data table. They will combine credible data, task-specific orchestration, transparent evidence, persistent monitoring, and a clear user segment. A product for an institutional credit desk will look very different from a product for an active retail equity investor, even when both use the same underlying model family.

Data providers gain leverage, but interfaces are being renegotiated

Agentic systems increase the value of clean financial data because an autonomous workflow can only be as reliable as the sources it retrieves. Structured fundamentals need correct period alignment. Estimates need source and timestamp awareness. Filings need accurate sectioning and table extraction. Transcripts need speaker attribution. News needs entity linking and event classification. A model can disguise weak data for a few paragraphs, but it cannot build a durable research product on top of inconsistent inputs.

At the same time, conversational and agentic interfaces weaken the old assumption that users must consume data through the provider’s traditional interface. A user may increasingly ask for a task—“show me which assumptions changed after earnings”—instead of navigating through a fixed set of pages. That creates tension and opportunity. Incumbent data providers can embed intelligence into their own products, license data to AI-native applications, or become invisible infrastructure behind new workflows. The interface layer becomes a strategic battleground because it controls user intent and the final decision context.

Model providers win volume, but finance demands specialization

Frontier model providers benefit as investment research consumes more inference, longer context, search, code execution, and tool calls. Multi-agent systems can multiply that usage. Yet finance also exposes the limits of generic intelligence. A model that writes elegantly may still mis-handle a restatement, confuse fiscal and calendar years, or compare non-equivalent metrics. Domain evaluation, retrieval design, calculation tools, and guardrails are therefore part of the product, not afterthoughts.

The likely equilibrium is not one finance model controlling the whole market. It is a layered system in which applications route tasks across models and tools. A fast model may classify documents. A stronger reasoning model may synthesize the thesis. Code may perform calculations. A retriever may handle filings. A deterministic rules engine may enforce portfolio or compliance constraints. The brand users see may be the workflow product rather than the underlying model.

AI-native platforms can win by owning the research object

The most interesting application-layer opportunity is to own the persistent research object: a living thesis that contains the original evidence, bullish and bearish arguments, valuation assumptions, risk triggers, and a record of what changed. Traditional chat interfaces are weak at this because conversations are ephemeral and unstructured. Traditional screeners are weak because they identify candidates but do not preserve a narrative. Research terminals are strong at data access but often require the analyst to assemble the thesis manually.

An AI stock agent can turn the thesis into a product surface. That object can be revisited after earnings, compared against new evidence, shared, challenged, and monitored. It can also drive retention: the user has a reason to return because the system knows what the user believed and can explain whether the facts still support it. This is where AlphaVue’s architecture is commercially relevant. Its public product positioning is centered on parallel agents, a verdict, bull-versus-bear debate, risk stress testing, evidence trails, and thesis-change alerts. The soft promotional case is not that AlphaVue has solved investing. It is that the platform is designed around the research object that agentic investing makes possible.

The strongest moat is calibrated trust, not artificial certainty

Investment products often market confidence, but the more durable moat may be calibrated trust. Users need to know when the system is confident, why it is confident, and what evidence would change the answer. They need source links and clear timestamps. They need calculations that can be reproduced. They need disagreement to remain visible when the evidence is genuinely mixed. They need the system to abstain when data is missing.

This is strategically important because finance punishes hidden errors. A consumer may forgive a creative assistant for a small mistake in a travel itinerary; an investor may abandon a platform after one fabricated revenue figure or one alert based on stale data. The products that build trust will therefore invest heavily in retrieval quality, provenance, evaluation, monitoring, and user control. Those investments may look less dramatic than a demo of an autonomous trader, but they are more likely to support recurring revenue.

What public-market investors should watch

Investors following the AI-investing theme should monitor several leading indicators. First, watch whether banks move agentic systems from pilots into governed production workflows and whether they disclose measurable productivity gains. Second, watch the economics of inference: lower model costs make multi-agent analysis more viable, while expensive long-running workflows can weaken consumer margins. Third, watch financial-data licensing and partnerships, because high-quality data can become a bottleneck. Fourth, watch regulation around model risk, recordkeeping, advice, and autonomous action. Fifth, watch user retention rather than launch headlines. A tool that generates a one-time report is interesting; a platform that becomes the investor’s recurring research desk has a stronger business.

The long-term opportunity is broader than stock picking. Agentic financial systems can support portfolio monitoring, advisor preparation, compliance review, credit research, due diligence, corporate finance, and risk operations. But public-equity research is a compelling entry point because the data is abundant, the user problem is intuitive, and the output can be evaluated against source documents. That makes AI stock agents both a product category and a proving ground for the wider automation of knowledge work in finance.

Related product sources: Bloomberg AI · AlphaVue · Fiscal.ai · Koyfin equity research

Limitations, Failure Modes, and Compliance Boundaries

Hallucination and false precision remain the primary product risk

The biggest failure mode in AI investing is not obvious nonsense. It is polished wrongness. Because financial writing is formulaic and numbers often look plausible when taken out of context, a model can sound extremely competent while misreading a footnote, using an outdated segment definition, or inventing a causal explanation not present in the source documents. Finance-specific research continues to treat hallucination as a core deployment barrier. Recent work such as FinBench-QA-Hallucination and K-FinHallu shows that hallucination detection in financial RAG is still challenging, especially under noisy or multi-turn conditions, while work on fine-grained knowledge verification is explicitly designed to push models toward claim-level faithfulness rather than fluent improvisation.

This is why grounded tools matter. Source-linked outputs, retrieval logs, evidence strings, click-through auditability, and forced abstention are not cosmetic. They are practical defenses against false precision. Seeking Alpha’s own help center openly warns that some AI-generated reports are not curated or reviewed by editors and may contain errors. That level of disclosure is healthy. It also suggests a broader rule for users: when an AI stock tool hides its evidence or refuses to show uncertainty, trust should go down, not up.

Stale data and retrieval gaps are more common than many users realize

A second failure mode is temporal mismatch. The model may retrieve an old filing, a pre-split share count, a prior segment taxonomy, or a stale macro fact. Even when a platform says data is updated rapidly, document latency can vary by source type. Fiscal.ai says company data updates within minutes of earnings, but also notes that transcripts and filings can take up to two days. TradingView and Koyfin are strong on market context and dashboards, but that does not automatically make them deep filing reasoners. Bloomberg’s and Seeking Alpha’s AI features are likewise constrained by the scope and recency of the content they index. In investing, a correct answer to last quarter’s question can still be the wrong answer today.

Backtest overfitting is the silent killer of “AI can beat the market” claims

When AI stock products move from research assistance into performance claims, the burden of proof rises sharply. Backtests can be accidentally or deliberately overfit through universe selection, prompt tuning on a known period, hidden survivorship bias, cherry-picked thresholds, or failure to model transaction costs and slippage. FinTradeBench’s finding that retrieval materially helps on textual fundamentals but only modestly improves trading-signal reasoning is a useful warning here. It suggests that many current systems are better at interpreting company narratives than at extracting live-edge prediction signals from price data. If a vendor’s marketing leaps from “better document understanding” to “superior stock picking,” skepticism is warranted.

Regulatory, supervisory, and ethical boundaries are tightening, not disappearing

Using AI does not exempt a firm or a product from finance regulation. FINRA’s 2024 notice reminded firms that existing rules remain in force when using generative AI and LLMs, including obligations around supervision, communications, books and records, and other technology-neutral requirements. The SEC’s 2026 speech on the future of investment management under AI likewise makes clear that regulators view the topic as both a source of opportunity and a source of substantive risk. In the UK, the Bank of England has gone further, explicitly linking AI capabilities to cyber and operational-resilience risks in its 2026 Financial Stability Report and discussing agentic AI’s implications for markets and payments.

For stock agents, one ethical boundary is especially clear: insider trading remains illegal whether the trader is human or model-assisted. The SEC states that illegal insider trading generally involves buying or selling a security on the basis of material nonpublic information, including tipping and trading by recipients of that information. An AI stock agent scraping internal emails, private Slack messages, or leaked documents would not create a loophole. It would create a more complex compliance failure. This is one reason enterprise agent systems are being designed around permissions, connectors, approval flows, and audit logs rather than unconstrained autonomy.

The correct strategic framing is augmentation with accountability

The right strategic frame for 2026 is neither “AI replaces analysts” nor “AI is just a toy.” It is “AI augments research, but the accountability stack must be explicit.” Anthropic’s guidance on effective agents, its work on context engineering, and its multi-agent research notes all support a design philosophy in which tool quality, context control, and evaluation rigor matter as much as base-model capability. OpenAI’s own product path from tool-using APIs to ChatGPT agent similarly broadens real-world utility while explicitly acknowledging novel risks. In finance, this means the best products will likely be those that combine workflow compression with clear evidence, bounded action, human override, and logged decision paths.

Research sources: FINRA Regulatory Notice 24-09 · SEC: AI and the future of investment management · SEC: insider trading · Bank of England AI work

How Investors Should Use AI Stock Agents Today

Use the agent to widen the funnel, not to outsource conviction

A disciplined investor can use an AI stock agent in four stages. The first stage is triage. Ask the system to identify the business model, major segments, current growth drivers, balance-sheet risks, and the most important recent disclosures. The goal is not to decide whether to buy. It is to decide whether the company deserves deeper work. This prevents the common mistake of spending hours on a stock whose core economics do not fit the investor’s mandate.

The second stage is evidence construction. Require the system to attach primary sources, distinguish reported facts from interpretation, and show the period associated with every important number. Ask it to compare management’s current language with prior calls. Ask where the bullish case depends on estimates rather than reported results. Ask which claims are disputed or uncertain. A useful agent should make the research easier to audit, not merely easier to read.

The third stage is adversarial analysis. Separate the bull and bear cases. Ask a risk agent to attack the thesis, not summarize generic risks. A good bearish case should identify specific mechanisms of failure: customer concentration, refinancing, margin normalization, regulatory limits, supply constraints, dilution, or expectations embedded in valuation. Then ask what evidence would falsify each side. This converts a narrative into a decision framework.

The fourth stage is monitoring. Save the thesis and define variables that matter. For a semiconductor company, those might include utilization, lead times, customer capex, gross margin, export restrictions, and product transitions. For a software company, they might include net retention, remaining performance obligations, seat growth, pricing, and AI monetization. The agent should alert the investor when those variables move—not every time the stock price changes.

A six-question reliability checklist

Can I open the source? Every decisive fact should point back to a filing, transcript, official release, or clearly identified dataset.

Is the timestamp visible? The system should make it difficult to confuse current information with an old quarter or outdated market price.

Are calculations reproducible? Ratios and scenario outputs should be generated with code or structured formulas, not trusted solely because a language model produced them.

Does the system show disagreement? A single polished answer can hide uncertainty. Bull, bear, and risk views reveal where the thesis is fragile.

Can it say “insufficient evidence”? Abstention is a feature in finance. A product that always reaches a strong conclusion is probably optimizing presentation over truth.

Does monitoring connect to the thesis? Alerts should explain which assumption changed and why it matters, rather than generating more noise.

What not to delegate

Do not delegate the investment mandate, risk budget, time horizon, liquidity needs, or responsibility for the decision. An AI agent does not know the full cost of being wrong for a specific investor. It may not understand tax constraints, concentration elsewhere in the portfolio, personal cash-flow needs, or the psychological risk of holding a volatile position. It can help structure the evidence, but the user must define what outcome is acceptable.

Do not treat a buy, hold, or sell label as a universal instruction. Such labels are only meaningful relative to assumptions, valuation, time horizon, and risk tolerance. The most useful role of the verdict is navigational: it summarizes the current balance of evidence and tells the user where to inspect disagreement. The evidence trail should remain more important than the label.

Finally, do not confuse research automation with market certainty. AI can reduce the probability of missing a disclosure, but it cannot eliminate surprise. It can model scenarios, but it cannot assign perfect probabilities. It can detect a thesis change, but it cannot guarantee that the market will price the change rationally or immediately. The disciplined use of AI stock agents is therefore not blind delegation. It is a better-controlled research process.

Frequently Asked Questions

What is an AI stock agent?

An AI stock agent is a goal-directed investing workflow built on top of models, tools, and data systems. In practical terms, it combines reasoning with actions such as retrieving filings, searching transcripts, running calculations, comparing bullish and bearish evidence, and monitoring watchlists over time. That is broader than a one-shot chatbot summary.

Are AI stock agents actually useful for investors?

Yes, especially for first-pass diligence, transcript digestion, filings retrieval, idea comparison, and ongoing monitoring. They are already being deployed in financial institutions for productivity and research-support workflows, but usefulness is highest when outputs are grounded in source documents and reviewed by a human.

Can AI stock agents replace human analysts?

Not reliably. Current research suggests that models have improved meaningfully on textual fundamentals and document QA, but still struggle more on numerical and trading-signal reasoning. The best current use is augmentation: compressing low-value research work while preserving human judgment and responsibility.

How do AI stock agents avoid hallucinations?

They reduce hallucinations by grounding answers in retrieved evidence, attaching citations or click-through source paths, using structured verification or code execution for calculations, and evaluating groundedness explicitly. New finance-specific research is focused exactly on these protections, because hallucination is a central deployment risk in financial AI.

What is the difference between RAG and a multi-agent system?

RAG is a method for retrieving external evidence and passing it into generation. A multi-agent system is an orchestration pattern in which multiple specialists or roles collaborate or debate before producing an answer. In finance, the two are often combined: one or more agents retrieve evidence, other agents analyze it, and a synthesizer produces the final memo.

Are AI stock agents legal to use?

Using them for public-data research is generally legal, but existing finance rules still apply. FINRA has reminded firms that regulatory obligations remain in force when using generative AI, and insider-trading rules still prohibit trading on material nonpublic information regardless of whether an AI tool was involved.

What should investors look for when choosing an AI stock tool?

Look for evidence visibility, source grounding, update cadence, alerting and monitoring support, workflow fit, and clarity about limitations. Marketing claims about “beating the market” matter less than whether the product can show you where its key conclusions came from.

Where does AlphaVue fit in this market?

AlphaVue fits the AI-native stock-research category. Its clearest differentiators, based on its public product pages, are parallel multi-agent analysis, bull-versus-bear debate, risk stress testing, evidence trails, and thesis-change alerts for public-market investors, all at a self-serve price point.

Research Sources and Further Reading

Google DeepMind — Gemini 3.5: frontier intelligence with action

FinanceBench: A New Benchmark for Financial Question Answering

FinBen: A Holistic Financial Benchmark for Large Language Models

Bank of England and FCA — Artificial intelligence in UK financial services 2024

SEC — Artificial intelligence and the future of investment management

AlphaVue — AI stock analysis and investment research platform